The global energy landscape is experiencing deep transformation. Overall, the global energy demand continues to increase, albeit at varying rates at the regional level. Demand in the countries of the European Union, the United States and other industrialized countries is either stabilizing or decreasing, whereas demand in other countries, namely China, India and other countries in Asia, is showing a sharp increase. Overall, the demand for energy is also increasing in the countries of the Middle East and North Africa (MENA), though significant differences can be observed between energy importing and energy exporting countries.

Thanks to their geographical location, the abundance of fossil fuel reserves in several MENA countries, the existing infrastructure and historical policy ties, MENA countries are embedded in the global energy order and have contributed to some extent to shaping it. However, recent socio-economic and political developments, coupled with major technology innovations in energy markets that have shifted attention away from the fossil energy reserves in the MENA region, are challenging the role traditionally played by MENA countries.

Several MENA countries are among the largest oil and natural gas suppliers globally, and as such, they are clearly embedded in the global energy system. However, their own growing energy needs that are challenging their export capacities could potentially impact their budget revenues. Some of the observed trends have been found to have a direct impact on the future role of MENA countries, whereas others are less relevant. The increasing trend of oil and gas demand growth is expected to continue, and thus is not foreseen to peak very soon.

Despite the unconventional fossil fuels revolution, especially in the United States, oil from the MENA region will be needed to fuel world economies. A real challenge for MENA countries, however, is the increasing domestic demand, which might jeopardize the region’s export capacities. In particular, the growth of the electric car market, though curbing oil demand in the transport sector, still is not replacing global oil demand and thus not challenging the export potential of oil producing countries. Moreover, the price of US unconventional oil is not yet competitive with the MENA supply.

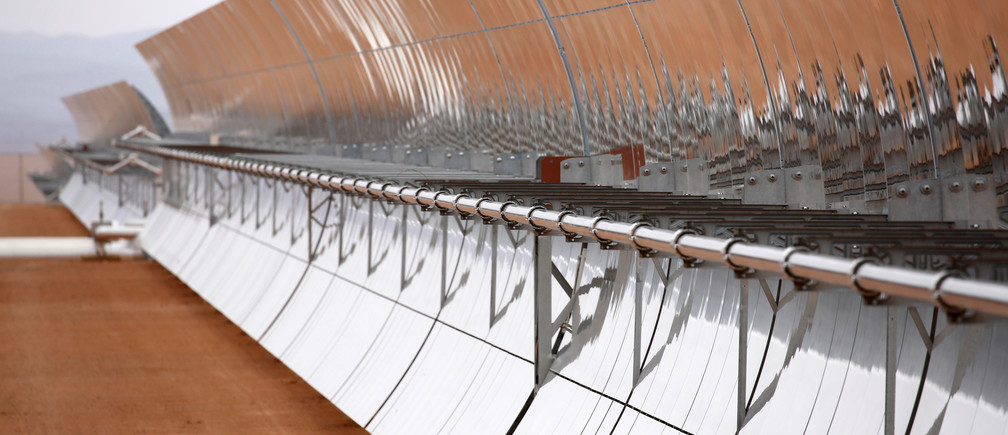

Conversely, the expanding market for LNG, with an increasing number of producers, is creating an excess of supply which could potentially challenge the export capacity of MENA countries. Another energy market segment in which MENA countries are lagging behind is renewable energy technologies. The use of renewables is expanding rapidly across the world, with the role of developing countries and economies in transition increasing in this sector. However, MENA countries are far from fully exploiting their potential when it comes to renewables.

Renewables could be a valid alternative to meet some of the challenges facing the MENA countries’ energy systems. However, their institutional and regulatory systems must evolve towards more business-oriented models. Some MENA countries have begun the transition towards sustainable energy, and several MENA companies are positioning themselves as key industrial players, even outside regional borders. But their speed of implementation will need to be accelerated further if MENA countries want to maintain leadership in the energy market and avoid becoming peripheral players.

‚The MENA Region in the Global Energy Markets‘ – Working Paper by Emanuela Menichetti, Abdelghani El Gharras, Barthélémy Duhamel and Sohbet Karbuz – Barcelona Centre for International Affairs / CIDOB.

(The Working Paper can be downloaded here)